Trump Account: A New Tax Savings Advantage for Children

College Planning Investing InsightsWhat Is a Trump Account?

A Trump Account is a brand-new type of custodial IRA for children, created under the One Big Beautiful Bill Act (signed into law in 2025). It is owned by the child but managed by a parent or guardian until the child turns 18. Accounts become available after July 4, 2026 — and unlike most retirement accounts, no earned income is required to contribute.

Key Highlights at a Glance

Who Qualifies?2

- Any child under age 18 with a valid Social Security number

- No earned income required

- No income limits for contributors

- One account per child only

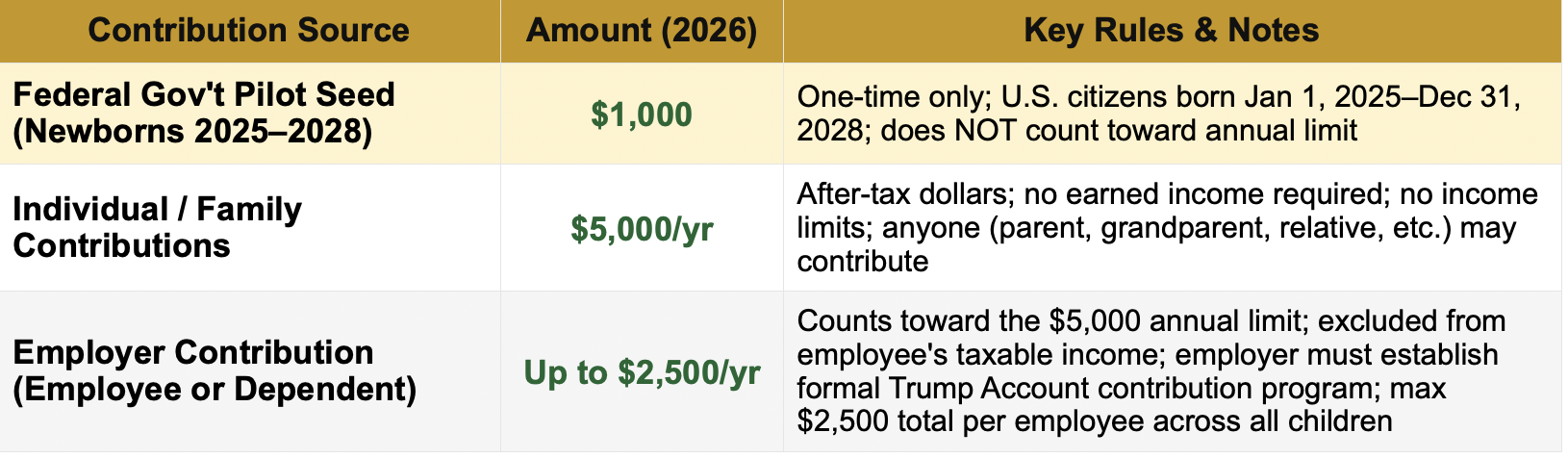

Who Can Contribute?2

- Parents, grandparents, relatives, friends

- Employers (up to $2,500/yr, excluded from taxable income)

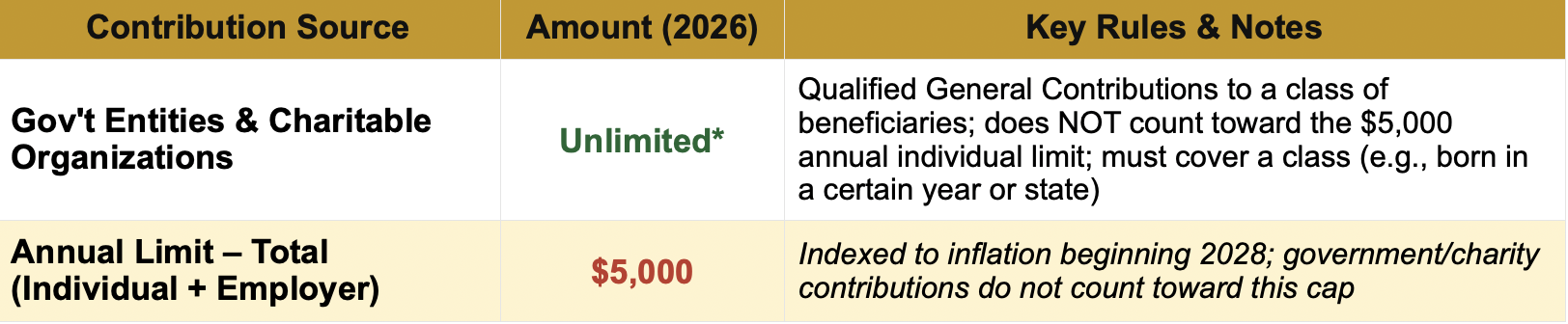

- Government entities & charities (outside annual limit)

- Federal government: $1,000 one-time seed for newborns 2025–2028

Tax Advantages2

- Contributions are after-tax (no deduction)

- Earnings grow tax-deferred inside the account

- Employer contributions excluded from employee’s taxable income

- Converts to traditional IRA at age 18 — tax-deferred growth continues

Withdrawal Rules2

- NO withdrawals before January 1 of the year child turns 18

- After age 18: traditional IRA rules apply

- Early withdrawal before 59½: 10% penalty applies

- Eligible disabled children may roll into an ABLE account

2026 Contribution Limits3

Annual limits are indexed to inflation beginning in 2028. Government and charitable contributions do not count toward the $5,000 annual cap.3

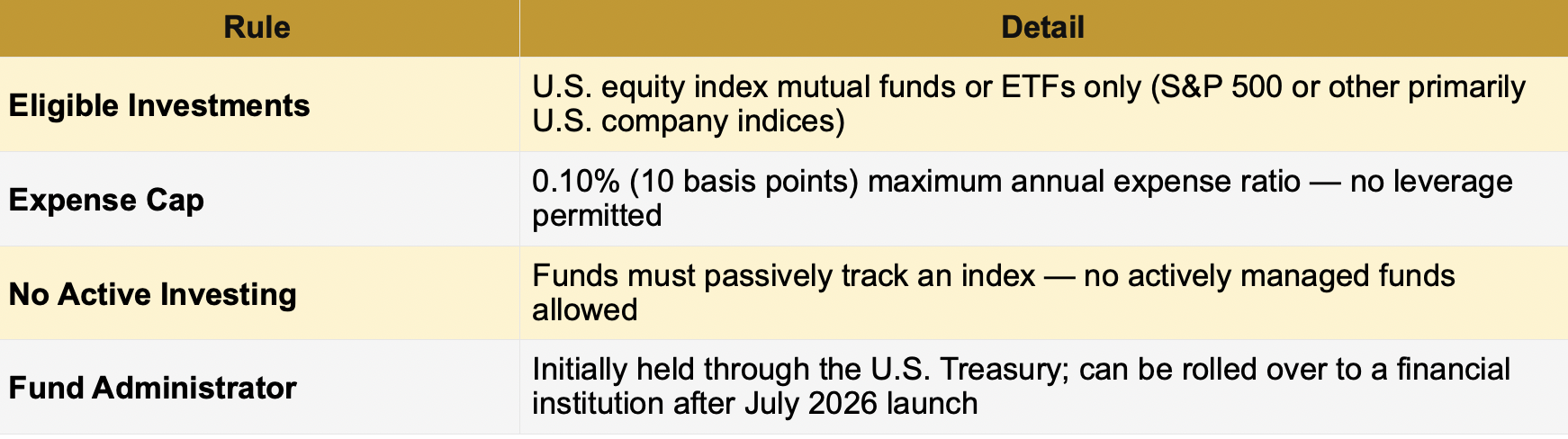

Investment Rules2

Important: No Existing IRA Transfers Permitted6

⚠️ Existing IRAs CANNOT be transferred or rolled into a Trump Account.

A Trump Account must be designated as such at inception — it is a new, standalone account. The following transfer types are not permitted:6

- A child’s existing custodial traditional IRA cannot be rolled over or converted into a Trump Account

- A child’s existing Roth IRA cannot be transferred into a Trump Account

- Trump Accounts cannot receive SEP or SIMPLE IRA contributions

- No partial rollovers — any trustee-to-trustee transfer must move the entire Trump Account balance

What IS allowed: A child may hold both a Trump Account and a separate traditional or Roth IRA simultaneously. They are independent accounts and contributions to one do not affect the limits of the other. The only permitted rollover is a full trustee-to-trustee transfer from one Trump Account trustee to another (e.g., moving from the initial Treasury account to a bank or brokerage after July 2026).

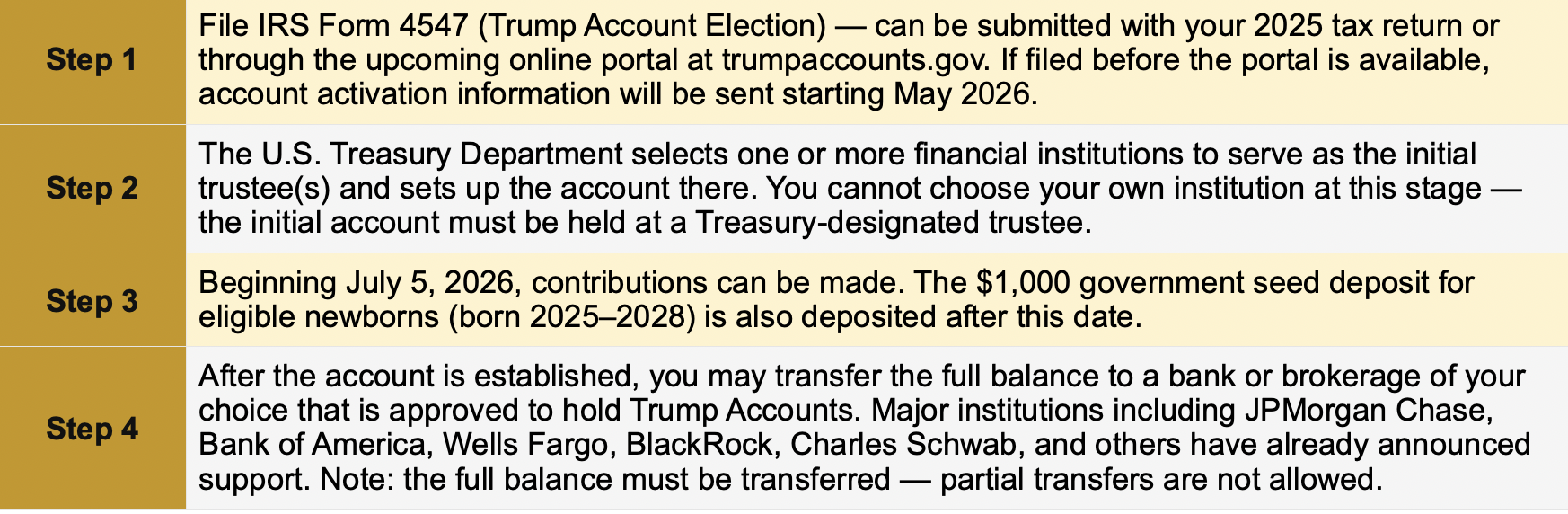

How to Open a Trump Account4,5

Can I open directly with a financial institution?

Not initially. All Trump Accounts must first be established through the U.S. Treasury’s designated trustee(s). Once that initial account exists, you may roll it over to your preferred bank or brokerage. Financial institutions are actively preparing to accept these rollovers after the July 2026 launch.7

Sources

1 One Big Beautiful Bill Act, Pub. L. No. 119-21 (2025) — Working Families Tax Cuts provisions establishing Trump Accounts.

2 IRS Notice 2025-68 — Treasury and IRS guidance on Trump Accounts (eligibility, contribution rules, investment requirements, distributions). irs.gov/pub/irs-drop/n-25-68.pdf

3 IRS Notice 2025-67 — 2026 Cost-of-Living Adjustments for retirement plans and IRAs (contribution limits, catch-up limits). irs.gov/pub/irs-drop/n-25-67.pdf

4 IRS Trump Accounts Overview & Form 4547 — irs.gov/trumpaccounts

5 U.S. Department of the Treasury — Trump Accounts portal (forthcoming): trumpaccounts.gov

6 IRS Notice 2025-68 & RSM US, "Treasury defines operating framework for new Trump accounts" (2026) — existing IRAs cannot be converted into Trump Accounts; account must be designated as a Trump Account at inception.

7 UBS, "What to know about Trump Accounts" (2026); Fidelity, "What are Trump Accounts and how do you open one?" (2026); America’s Credit Unions, "Trump Accounts" (2026) — all initial accounts must be opened through Treasury-designated trustee(s); rollovers to preferred banks or brokerages permitted after July 5, 2026.

Securities offered through Cetera Wealth Services, LLC, member FINRA/SIPC. Advisory Services offered through Cetera Investment Advisers LLC, a registered investment adviser. Cetera is under separate ownership from any other named entity. For a comprehensive review of your personal situation, always consult with a tax or legal advisor. Neither Cetera Wealth Services, LLC nor any of its representatives may give tax or legal advice. All investing involves risk, including the possible loss of principal. Kyle Williams, Financial Advisor, CRPC® 731-431-1100, kyle@401kyle.com, 8 Mason Road, Three Way, TN 38343.

Distributions from traditional IRAs and employer sponsored retirement plans are taxed as ordinary income and, if taken prior to reaching age 59 ½, may be subject to an additional 10% IRS tax penalty. Some IRAs have contribution limitations and tax consequences for early withdrawals. For complete details, consult your tax advisor or attorney. Tax Deferral - 10% IRS penalty may apply to withdrawals prior to age 59 ½.

Important: This document is for informational purposes only. It does not constitute tax, legal, or financial advice. Trump Account regulations are still being finalized (IRS Notice 2025-68); consult a qualified tax professional before making account decisions.