Planning for Healthcare Before And At Medicare Age 65

Retirement Funding InsightsOne of the most common questions I hear from clients approaching retirement is, “Kyle, what do I do about health insurance?” It’s a fair question — and the answer depends a great deal on when you plan to retire.

At 401Kyle.com, we believe it’s better to prepare than to repair. That same principle applies directly to healthcare planning. Whether you’re retiring at 58, 62, or exactly at 65, understanding how Medicare works — and what you need before it starts — is one of the most important pieces of your overall retirement readiness.

Retiring Before 65: Bridging the Gap

Medicare eligibility begins at age 65 for most Americans. If you plan to retire before that birthday, you’ll need to bridge the coverage gap on your own. This window can last anywhere from a few months to a full decade, and the costs can be significant.

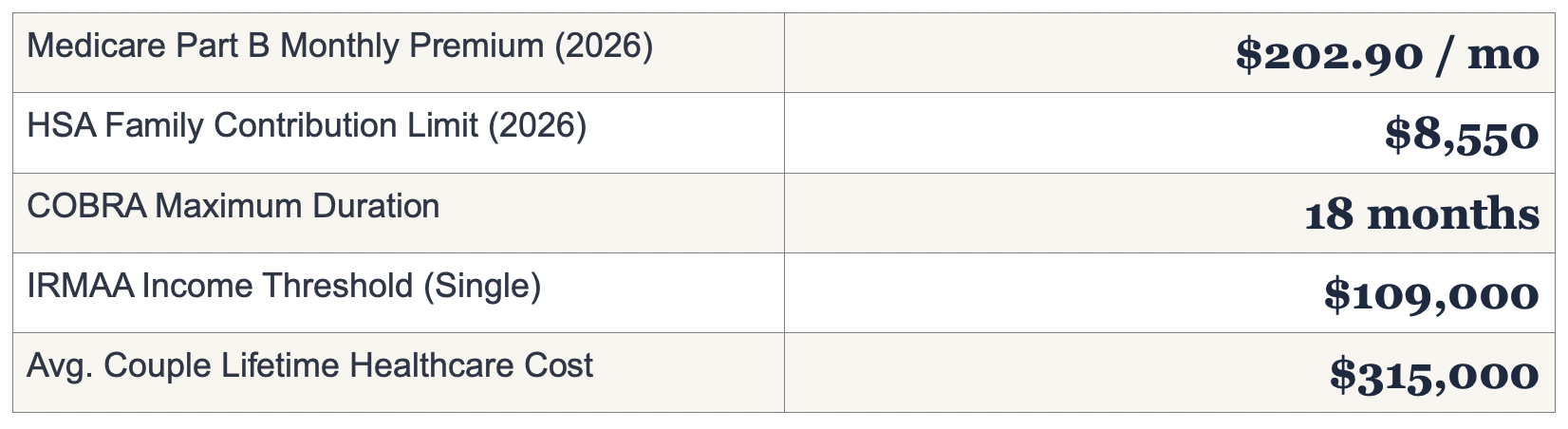

The most common paths for coverage during this period are COBRA continuation from your former employer (available for up to 18 months), enrollment in an ACA Marketplace plan through Healthcare.gov, or joining a spouse’s employer plan if they are still working. Each option carries different costs, network limitations, and tax implications — which is why we build healthcare cost projections directly into your retirement income plan.

Turning 65: Understanding Medicare

Medicare is the federal health insurance program for Americans age 65 and older. It is made up of distinct parts. Part A covers hospital stays and is generally premium-free with 10+ years of work history. Part B covers doctor visits and outpatient services, with a standard monthly premium of $202.90 in 2026.

From there, you choose how to supplement your coverage: through a Medigap (Medicare Supplement) policy that covers out-of-pocket gaps, or a Medicare Advantage (Part C) plan that bundles benefits through a private insurer. You’ll also want to evaluate a Part D prescription drug plan — because skipping it, even briefly, results in a permanent penalty added to your premium for life.

One number that surprises many clients is the IRMAA surcharge — a higher Part B and Part D premium triggered when your income from two years prior exceeds certain thresholds. This is exactly why we review your income strategy holistically, including how Roth conversions and capital gains in the years leading up to 65 can affect your Medicare costs.

The Role of a Health Savings Account (HSA)

If you are currently enrolled in a high-deductible health plan, maximizing your HSA contributions before retirement is one of the smartest moves you can make. HSA funds grow tax-free, withdraw tax-free for qualified medical expenses, and can even be used to reimburse Medicare premiums in retirement. It functions as a dedicated, tax-advantaged healthcare reserve — one of the few true “triple tax” benefits in the tax code.

At 401Kyle.com, healthcare cost planning is woven into every retirement income strategy we build. Tomorrow is not promised — but a well-prepared plan means you can face whatever comes with confidence. Let’s make sure your healthcare picture is as clear as your investment strategy.

KEY NUMBERS TO KNOW

Ready to Build your Healthcare Retirement Plan?

Schedule a conversation with Kyle Williams today at 401Kyle.com - because healthcare is your biggest retirement wildcard.

DISCLOSURES

Securities offered through Cetera Wealth Services, LLC, member FINRA/SIPC. Advisory Services offered through Cetera Investment Advisers LLC, a registered investment adviser. Cetera is under separate ownership from any other named entity. For a comprehensive review of your personal situation, always consult with a tax or legal advisor. Neither Cetera Wealth Services, LLC nor any of its representatives may give tax or legal advice. All investing involves risk, including the possible loss of principal. Kyle Williams, Financial Advisor, CRPC® · 731-431-1100 · kyle@401kyle.com · 8 Mason Road, Three Way, TN 38343.

This blog is for educational and informational purposes only.

Individual healthcare needs and eligibility vary. Converting from a traditional IRA to a Roth IRA is a taxable event. A Roth IRA offers tax free withdrawals on taxable contributions. To qualify for the tax-free and penalty-free withdrawal or earnings, a Roth IRA must be in place for at least five tax years and distribution must take place after age 59 ½ or due to death, disability or a first-time home purchase (up to a $10,000 lifetime maximum) Depending on state law, Roth IRA distributions may be subject to state taxes.