Give Smarter: How to Use Your IRA to Support Charity

Investing Retirement Funding InsightsIf you are charitably inclined and have money sitting in an IRA, there is a powerful strategy worth knowing about: the Qualified Charitable Distribution, or QCD. Rather than taking a taxable withdrawal and then writing a check to your favorite charity, a QCD allows eligible IRA owners to transfer funds directly to a qualified nonprofit — and exclude that amount from their taxable income. It is one of the most tax-efficient charitable giving tools available for retirees.

What Is a Qualified Charitable Distribution (QCD)?

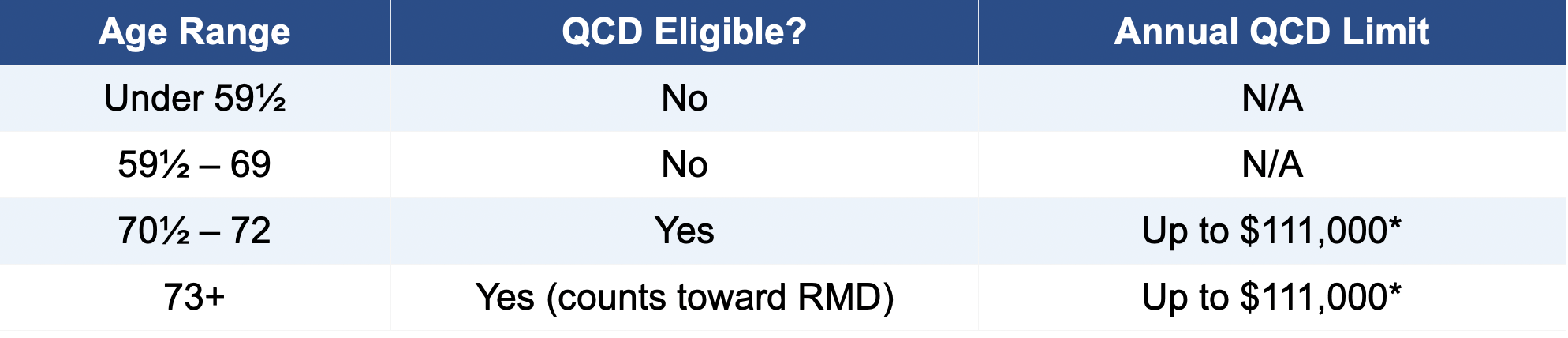

A QCD is a direct transfer from your traditional IRA to a qualified 501(c)(3) charity. For those age 70½ or older, up to $111,000 per year (2026 figure, indexed for inflation) can be transferred tax-free. For married couples, each spouse may contribute up to the limit from their own IRA. Importantly, if you are subject to Required Minimum Distributions (RMDs), a QCD counts toward satisfying your RMD for the year — helping you avoid that income hitting your tax return altogether.

IRA Charitable Gift Age Guide

Eligibility for QCDs depends entirely on your age:

* QCD limit is indexed for inflation and is $111,000 per individual for 2026 ($222,000 for married couples, each from their own IRA). Consult your tax advisor about current limits. Source: Give From Your IRA | AARP Foundation

Why a QCD Often Beats a Regular Charitable Deduction

Many retirees take the standard deduction, which means charitable gifts made by check provide no additional federal tax benefit. A QCD sidesteps this issue entirely. Because the distribution never appears in your adjusted gross income (AGI), it reduces the taxable income used to calculate Medicare premiums (IRMAA), the taxation of Social Security benefits, and other income-based thresholds. Simply put, giving through your IRA can be more powerful than writing a check — even if the dollar amounts are identical.

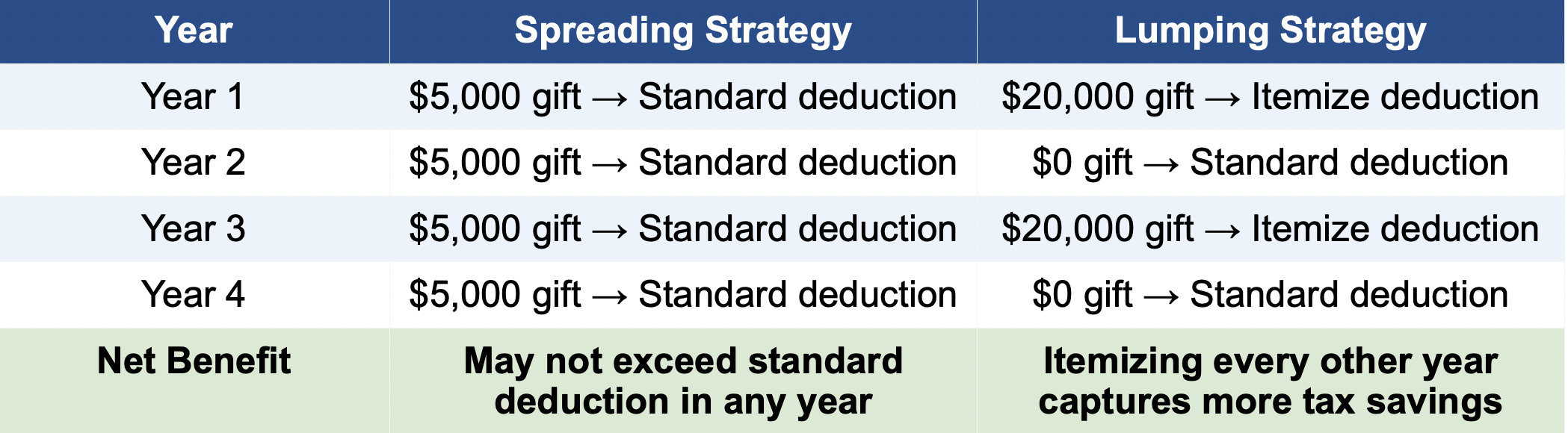

The Power of "Lumping" Charitable Gifts

For those not yet at QCD age — or who give primarily through cash — a strategy called "lumping" or "bunching" charitable gifts can help you take advantage of available tax deductions. Instead of giving a modest amount every year and relying on the standard deduction, you front-load two or more years of giving into a single tax year, allowing you to itemize that year and capture a larger deduction. The following year you revert to the standard deduction. The chart below illustrates this concept:

Note: Standard deduction amounts change annually. This example is for illustrative purposes only. Consult a tax advisor before implementing any gifting strategy.

Next Steps

Whether you are using a QCD to satisfy your RMD tax-free, or bunching gifts to maximize a deduction in a high-income year, charitable giving strategies are worth a conversation. Every situation is different, and the right approach depends on your age, income, tax bracket, and giving goals.

To explore how these strategies might fit into your overall retirement plan, reach out to Kyle Williams at 731-431-1100 or kyle@401kyle.com.

DISCLOSURES

Securities offered through Cetera Wealth Services, LLC, member FINRA/SIPC. Advisory Services offered through Cetera Investment Advisers LLC, a registered investment adviser. Cetera is under separate ownership from any other named entity. For a comprehensive review of your personal situation, always consult with a tax or legal advisor. Neither Cetera Wealth Services, LLC nor any of its representatives may give tax or legal advice. All investing involves risk, including the possible loss of principal. Kyle Williams, Financial Advisor, CRPC® 731-431-1100, kyle@401kyle.com, 8 Mason Road, Three Way, TN 38343.

This blog is for educational and informational purposes only.

Distributions from traditional IRAs and employer sponsored retirement plans are taxed as ordinary income and, if taken prior to reaching age 59 ½, may be subject to an additional 10% IRS tax penalty. Some IRAs have contribution limitations and tax consequences for early withdrawals. For complete details, consult your tax advisor or attorney. Tax Free - Income may be subject to local, state and/or the alternative minimum tax